Blue Cross Liable for Denied Treatment

By Natalie White From Lawyers Weekly June 6, 2005

A Louisiana jury recently ordered a health care insurer to pay a 33-year-old woman more than $2 million for denying diagnostic tests that would have detected a spinal tumor before it crippled her. It was the first time such an award under a little-known state statute holding insurers responsible for results of irresponsibly denying claims, said the plaintiff’s attorney,

Paul A. Lea, Jr. Lea said he was able to show the jury “how a condition which pre-existed the policy was not legally pre-existing condition.” He said jurors in conservative St. Tammany Parish, known for its slow verdicts, were outraged by the callous treatment. Blue Cross vice president John Maginnis said in a statement that the company denied the claim because “in the opinion of a number of board-certified physicians, her medical condition existed before her effective date of coverage.”

Furthermore, the Maginnis statement asserts that when the plaintiff applied for coverage, she failed to disclose the treatment she had received for her back pain. He said insurance companies must be diligent in denying coverage for pre-existing conditions because failure to do so would unfairly raise insurance rates for all policyholders. He indicated the company plans to appeal the verdict.

Denied Coverage

Christiane Hymel went to a neurologist because she was experiencing numbness, tingling and a general loss of sensation. The doctor told her that he suspected that her symptoms were caused by multiple sclerosis, but that he wanted to rule out a spinal tumor first. But Blue Cross Blue Shield refused to pay for the test saying that Hymel, newly insured was not entitled to coverage because she had a pre-existing back condition. As a result, Hymel was forced to wait three months while he saved money to pay for the $4,000 MRI. The unnecessary delay allowed an undetected spinal tumor to grow so large that, by the time it was detected, Hymel was in a wheelchair and needed immediate emergency surgery.

After months of intensive physical therapy, Hymel has managed to regain her ability to walk, although she has permanent nerve damage and numbness from her chest down, said Lea, who tried the case with Silvia Muller and Scott Gardner. Lea said the decision to deny coverage was made on faulty information and did not meet the standards of thorough investigation, as required by law. He argued that the company denied the claim without a proper investigation, directly violating a state statute. If official had done a proper inquiry, Lea said they would have discovered Hymel’s request had little to do with previous back pain.

Pre-Existing Condition?

Shortly after becoming a Blue Cross Blue Shield subscriber, Hymel went for a physical with her primary care doctor. She was not complaining of anything specific, Lea said. During the checkup, she mentioned back she had been experiencing on and off for a few years, but noted that it had been alleviated by chiropractic care. He suggested they get back x-ray.

The doctor also said he was concerned that she had a few areas of non-sensation in her hands and wanted her to see a neurologist. Hymel went to see the neurologist, who said he suspected she might have multiple sclerosis because of her intermittent and fleeting symptoms of numbness and tingling. However, he said he wanted to also rule out a spinal tumor and said she needed an MRI of her back, Lea said.

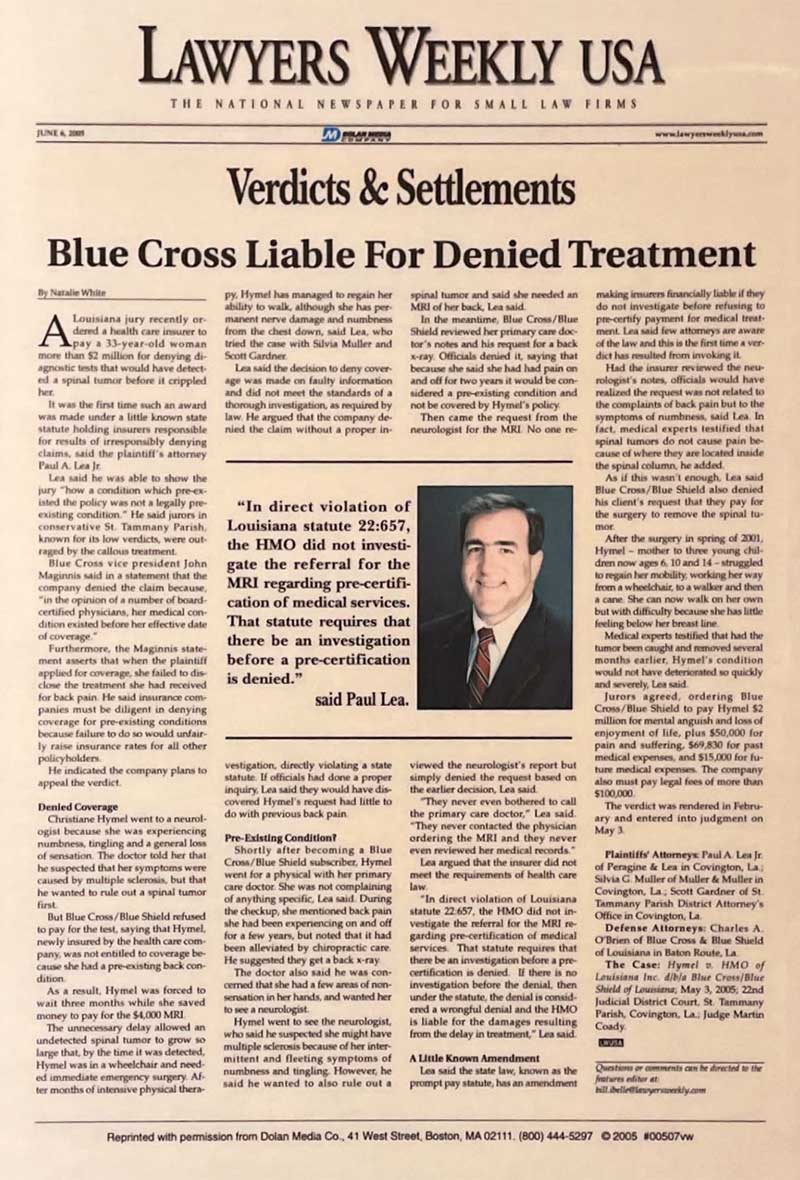

Then came the request form the neurologist for the MRI. No one reviewed the neurologist’s report but simply denied the request based on the earlier decision, Lea said. “They never even bothered to call the primary care doctor,” Lea said. “They never contacted the physician ordering the MRI and they never even reviewed her medical records.”Lea argued that the insurer did not meet the requirement of health care law. “In direct violation of Louisiana Statute 22:657, the HMO did not investigate the referral for the MRI regarding pre-certification and medical services.

That statute requires that there be an investigation before pre-certification is denied. If there is no investigation before the denial, then under the statute, the denial is considered a wrongful denial and the HMO is liable for the damages resulting from the delay in treatment,” Lea said.